The first step in credit repair involves obtaining your credit report. Your credit report holds the key to uncovering errors, omission, and inconsistencies.

By law each major credit bureau is required by law to regularly provide you one free credit report, when requested.

You can request your credit report from Annual Credit Report Request Service online, via phone, and by mailing:

Online: www.annualcreditreport.com

Phone: 1-877-322-8228

Address:

Central Source LLC

P.O. Box 105283

Atlanta, GA 30348-5283

Your report will provide you your credit history, credit cards, open and closed accounts, collection agencies, bankruptcies and foreclosures.

If you can no longer obtain your free credit report after initially obtaining it you can easily purchase copies.

Once you receive your credit report, review it closely for errors. A 2021 consumer report study found that more than 33% of study participants had at least one error on their credit report. These error can hinder a person from obtaining credit, home financing, and car financing. Checking your credit report regularly will help you achieve your credit score goals and fix errors.

When analyzing your credit report for errors, look for the following:

1. Incorrect personal information, including addresses and misspellings.

2. Missing accounts that should be listed on your report.

3. Inaccurate or false accounts.

4. Accounts that display "closed by grantor" (the lender closed the account).

5. Delinquencies and/or derogatory marks

6. Fraudulent activity

7. Data management errors

8. Incorrect inquires

Any of the above errors can damage and impact your score. This can lead to denials of credit and hinder your financial growth. If you find errors on one report, check the other reports for the same error.

Once you have identified the errors and mistakes in your credit reports, it is imperative to challenge them. By law the bureaus are obligated to remove and resolve any dispute. However, this is a process that requires you to take the first action by disputing the mistake via online, mail or phone.

To dispute the inconsistencies you will have to provide documentation proving your identity and documents substantiating your claim of unfair and inaccurate accounts or derogatory marks.

Equifax:

Online: Equifax Dispute Center

Phone: 866-349-5191

Mail: Equifax Information Services LLC

P.O. Box 740256, Atlanta, GA 30374

Experian:

Online: Experian Dispute Page

Phone: 800-916-8800

Mail: Experian

P.O. Box 4500, Allen, TX 75013

TransUnion:

Online: TransUnion Dispute Center

Phone: 800-916-8800

Mail: TransUnion Consumer Solutions

P.O. Box 2000, Chester, PA 19016

Pro-Tip: Contact the creditor and.or lender that issued the count to provide notice of your dispute and/or inaccuracies. In most cases, the lender had the ability to correct the information on their end. After contacting the bureaus you should response within 30 to 45 days. If not, continue to follow-up until you do.

Your credit report will also indicate late and overdue balances on your account. A payment is not considered late until a payment is 30 days past due.

Once an account is past 30 days late, creditors and lenders can report the late account to all three bureaus, which can impact your score and creditworthiness for up to 7 years.

Have a overdue account, there are ways to help get late payments and negative items removed.

Your account may be turned over to a collection agency after 30 days. A collection agency is sold the past due account for pennies on the dollars and will seek to obtain the full amount plus interest on the account. When the account is sold to a collection agency, it is indicated on your credit report.

Collection agencies make money by harassing creditors for payments. In turn your credit score will take a hit. If the balance is high, a collection agency may file suit against you to obtain a judgment.

A pay to delete agreement is a contract between a consumer and a collection agency to remove collection accounts from the consumer's report as long as the terms for the deletion are met. Typically, the terms require that the sum agreed upon is paid in full.

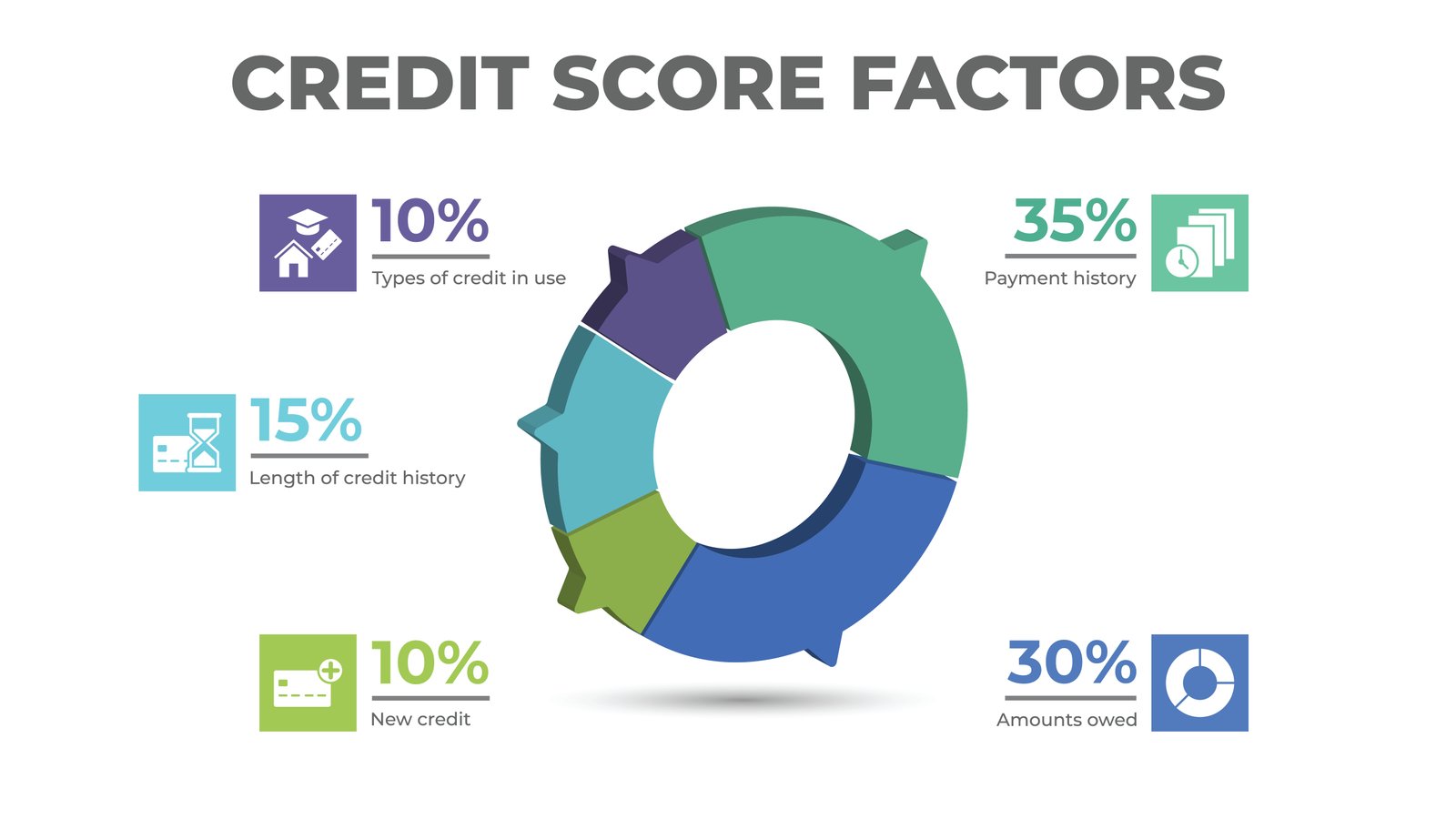

Credit utilization is the amount of money borrowed compared to the consumers credit limit. Credit utilization accounts for about 30% of your FICO score. You want to aim to keep your credit utilization below 30%. You can achieve this goal by paying down debt, increasing credit limits and keep card in an open status.

Credit cards are not always a bad thing and can be helpful when used responsibly and in emergencies. They can also help you build credit and make big purchases.

Lower credit utilization is a positive indicator to lender as it shows you are only using small amounts of credit.

Use this method to calculate credit utilization ratio:

1. Add up the amount of revolving credit you have (balance)

2. Add up the balance available to you (credit limit)

3. Divide the total balance by the credit limit.

4. Multiply that number by 100 to get a percentage.

A credit limit is the maximum amount that a person can spend before the balance is paid off. Credit limits vary by a few hundred and a few thousand dollars.

You can request that a lender or credit card company increase it by requesting it. A credit card company may review your file and increase your limit automatically without additional paperwork demonstrating your creditworthiness.

Think long term when making the decision to take out a loan or open a new credit account. Short term decision relating to credit can lead to hard inquiries (also known as a hard credit check).

When you have too many hard inquires in a short period of time, creditors see this a risky behavior and it will negatively impact your credit score.

Multiple checks for vehicles and a loan, like a mortgage or student loan, grouped in a short period of time will mostly be counted as a single in inquiry. Your credit will take less of a hit when this occurs.

Keeping long standing account open will be considered in your overall credit age. The older your credit history the better. Old accounts that display healthy payment history will make you appear more creditworthy.

Each client is different and the timeframe will differ. Once we assess your report we began work to avoid any delays in restoring your credit. We have seen thousands of removed inquiries to our clients that stay with us for six months.

We do not guarantee fast repair because that is realistic and companies that offer this type of service is likely engaging in illegal tactics for temporary results and could negatively affect your credit report even more.

No, in fact all three credit bearues encourage you to check your credit score regularly to ensure your report is accurate. A soft credit pull does not harm your score.

However, a hard inquiry will. This occurs when you apply for a new line of credit. Multiple inquires in a short time may have a negative impact on your credit score.

Negative inquires usually last seven to ten years. However, the credit bureaus have the ability to choose to delete negative credit history immediately when given a valid reason to do so.

Yes. You can hire a credit repair company to help you dispute negative and inconsistent item that are hurting your credit scores.

Reputable credit repair company cannot help you repair your credit overnight or guarantee the removal of accurately reported items. Please be careful about company that advertise fast and quick credit score increases.